Bridge Financing

Ready to accelerate your clean energy transition without breaking the bank? The Inflation Reduction Act (IRA) of 2022 offers significant new tax credits for governmental organizations and nonprofits for clean energy projects like solar, batteries and geothermal heat pumps, covering up to 30-70% of the project cost. But the timing can be a challenge. Nonprofits, tribal, and other government organizations often face the dilemma of funding up-front costs for projects while waiting for tax credit refunds. Michigan Saves is piloting a financing program that provides affordable short-term bridge funding for qualifying clean energy improvements under the IRA. This financing prefunds the estimated investment tax credit for eligible upgrades, with the funding paid back in full when the credit is received from the Internal Revenue Service.

This means you can start and complete your clean energy project without the financial burden of up-front costs.

How Does the Process Work?

Tell us a little about your project by completing this interest form. Then, work with a Michigan Saves authorized contractor for commercial loans to identify a qualified project and apply for the financing.

To initiate the financing application, submit the following to Michigan Saves via our lending partner, TEAM financial, at will.bulkowski@teamfinancial.com

- Proof of 501(c)(3) status

- Project scope of work, cost estimate, and schedule

- Description of tax credits being sought (contact Michigan Saves or Team Financial Group for more information)

- Copy of application to utility to interconnect solar facility

Upon review of these materials, Michigan Saves or Team Financial Group may follow up for additional underwriting documentation, including, but not limited to:

- Two years of financials (audited, compiled, or reviewed)

- Approval from governing body

- Applicable permits

- Evidence of borrower’s contribution

- Articles of incorporation and/or bylaws

Upon loan approval and closing, the contractor proceeds with installation of energy improvements, with Michigan Saves disbursing the loan amount in two installments (final installment after the project is in service).

The borrower will file for applicable tax credits in the first year after the project is operational and pay back the Michigan Saves loan when the tax credit is received or 24 months, whichever is sooner.

Bridge Financing Facts

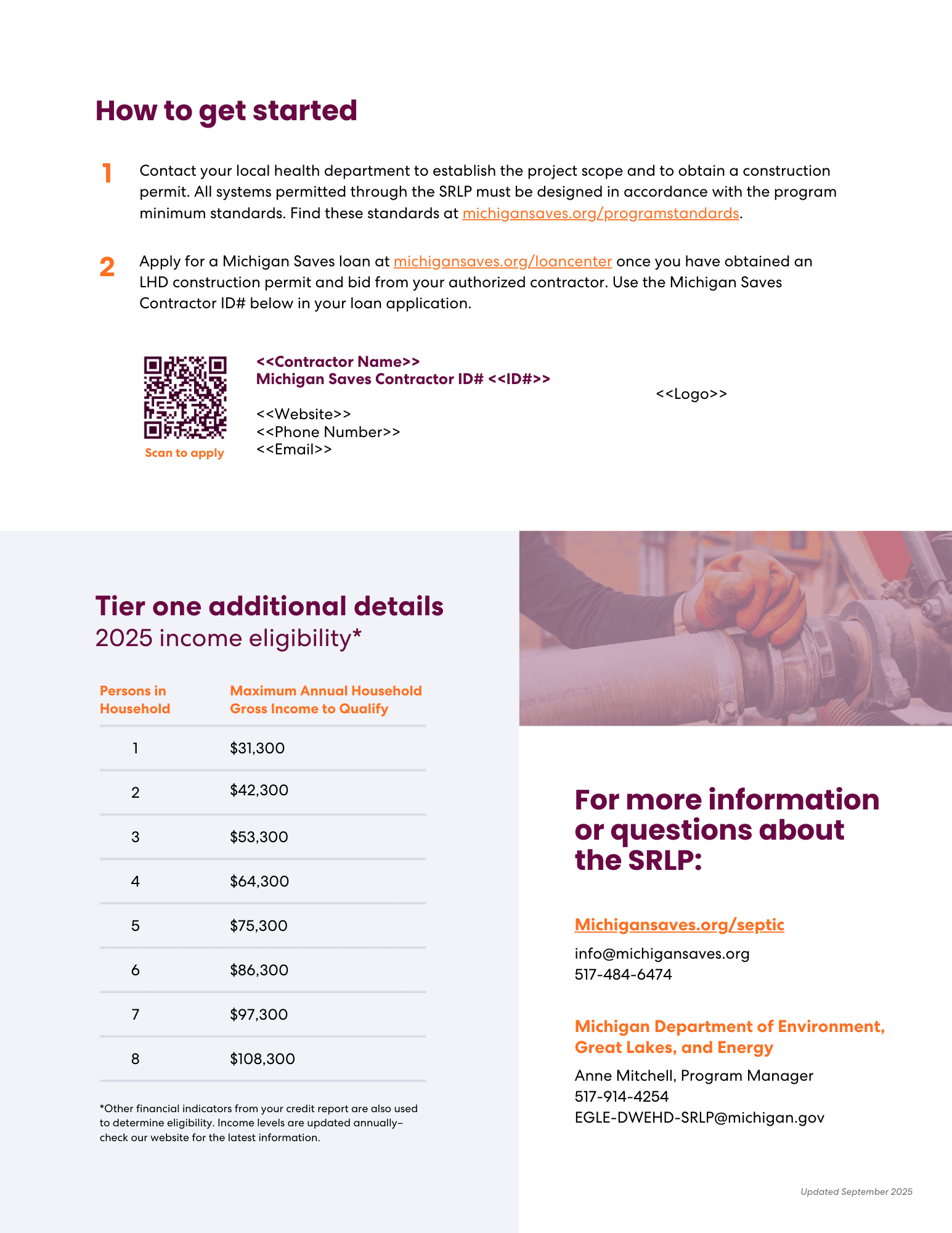

Eligible properties and entities: Facilities owned or operated by nonprofit organizations and governmental entities (e.g., local, state, and tribal governments and public school districts) eligible for direct pay tax credits under the IRA.

Eligible measures: Solar (less than 1 megawatt in nameplate capacity), geothermal heat pumps and battery storage that are eligible for the ITC. No minimum utility bill savings required unless needed for specific low-income tax credit bonuses.

Financing amount and term: $20,000–$250,000

Term: Upon receipt of direct pay credits with maximum term of 24 months

Interest rate: 3.99% APR

Fees and expenses: 1% origination fee and $250 documentation fee

Collateral: Proceeds from direct pay tax credits for financed project as set forth in financing agreement and a UCC filing on the equipment

Please note: Michigan Saves will not make a determination of your organization’s eligibility to earn the ITC or direct pay and recommends seeking input from a qualified tax expert to navigate the available tax credits.

Are you interested in bridge financing?

Frequently Asked Questions

Background on Entities and Measures Eligible for Michigan Saves Bridge Financing

What is the Michigan Saves Bridge Financing program?

The Inflation Reduction Act of 2022 reauthorized and expanded a wide array of clean energy tax credits through 2033 and allowed, for the first time, tax-exempt entities to directly access those tax credits through a process called direct pay (or elective pay). Qualifying entities can now receive a direct payment from the Internal Revenue Service in lieu of a tax credit. However, the IRS does not release the direct payment to the tax-exempt entity until after the organization has filed its tax return (i.e., Form 990) for the tax year in which the property is placed in service, forcing the tax-exempt entity to pay for the project up front and in full. Through the bridge financing program, Michigan Saves prefunds the portion of the project cost covered by the estimated tax credit for eligible upgrades, with the customer repaying the financing in full when they receive the credit from the IRS or 24 months after closing the loan, whichever is sooner. This means that the entity only raises funds for a portion of the project cost, with the bridge financing covering the rest.

What entities are eligible for the Michigan Saves Bridge Financing program?

The Michigan Saves Bridge Financing program is available to tax-exempt nonprofit and governmental entities, such as:

- Nonprofit organizations (including, but not limited to, houses of worship and nonprofit charter schools)

- Local, state, and tribal governments

- Public school districts

The IRS’s final regulations address the specific types of nonprofit organizations that qualify. As explained by the IRS:

The final regulations provide that any organization described in sections 501 through 530 that meets the requirements to be recognized as exempt from tax under those sections is eligible for elective pay. This includes, among others, all organizations described in section 501(c), such as public charities, private foundations, social welfare organizations, labor organizations, and business leagues. It also includes homeowners associations exempt under section 528.1

For-profit entities are not eligible for this program.

[1] Internal Revenue Service. August 20, 2024. “Elective Pay and Transferability Frequently Asked Questions: Elective Pay.” Irs.gov. https://www.irs.gov/credits-deductions/elective-pay-and-transferability-frequently-asked-questions-elective-pay#eligibility

My organization does not pay federal income taxes, so how would I be eligible for the direct pay investment tax credit?

Direct pay is a provision available under the Inflation Reduction Act to benefit tax-exempt organizations that install clean energy projects like solar and battery storage at their facilities. Previously, the credits were available only to third parties that contracted with a tax-exempt customer; under this model, there was not a requirement that such tax benefits flow to the tax-exempt customer. The direct pay model provides direct access to the tax credits with no intermediary. Tax-exempt organizations will still need to pay up front for the project, with the tax credit received after filing their Form 990 with the IRS the following year. Thus, Michigan Saves offers low-cost, streamlined financing to bridge this gap.

What types of improvements can be financed through the Michigan Saves Bridge Financing program?

The following measures are eligible for direct pay and the Michigan Saves Bridge Financing program:

- Solar photovoltaic (PV) systems

- Ground source heat pumps, a.k.a. geothermal systems

- Battery energy storage

Direct pay is available for other technologies, such as wind, hydro, biomass, and hydrogen. Entities interested in financing such projects should contact Michigan Saves to explore financing options.

Direct pay is available for other technologies, such as wind, hydro, biomass, and hydrogen. Entities interested in financing such projects should contact Michigan Saves to explore financing options, including the Michigan Saves Climate Fund.

Can I finance energy efficiency improvements or air source heat pumps?

No, not as part of the bridge financing program. However, Michigan Saves’ lending partner, Team Financial Group, has financing available for such measures with flexible terms. Contact Michigan Saves for more information to match the right financing program for your project.

I completed a solar project earlier this year and plan to apply for direct pay. Can I still use the Michigan Saves Bridge Financing?

No. However, Michigan Saves can provide financing for projects that are ready to execute or have started construction.

Rates, Terms, and Fees

What is the interest rate?

The current interest rate is 3.99%.

What is the maximum term available?

The maximum term is 24 months. This should provide sufficient time to complete the project and receive direct pay from the IRS. Even if you complete the project early in year one (e.g., February) and file an extension with the IRS the following year, the 24-month maximum term should be sufficient.

Are fees charged for this program?

There is a 1 percent origination fee and $250 documentation fee.

What is the maximum amount I can finance?

Financing is available for up to $250,000 through the Michigan Saves Bridge Financing program. If your financing needs exceed this amount, please contact Michigan Saves to explore other low-cost financing options, such as commercial term loans.

How the Process Works

How do I apply for the Michigan Saves Bridge Financing program? What information is needed?

The first step is to tell us a little about your project by completing this interest form. Then, work with a Michigan Saves authorized contractor for commercial loans to identify a qualified project and apply for the financing. To initiate the financing application, submit the following to Michigan Saves via our lending partner, Team Financial Group, at will.bulkowski@teamfinancialgroup.com:

- Proof of tax-exempt status

- Project scope of work, cost estimate, and schedule

- Description of tax credits being sought (contact Michigan Saves for more information)

- Copy of application to utility to interconnect the solar facility, if applicable

Upon review of these materials, Michigan Saves or Team Financial Group will follow up for additional underwriting documentation, including, but not limited to:

- Two years of financials (audited, compiled, or reviewed)

- Approval from the entity’s governing body

- Applicable permits

- Evidence of borrower’s contribution

- Articles of incorporation and/or bylaws

Do I need to work through a Michigan Saves authorized contractor to access the bridge financing program? How do I find one?

Yes. Michigan Saves requires its financing to be facilitated through a network of authorized contractors with expertise in solar, building science, or other energy-related improvements. You can find an authorized contractor at www.michigansaves.org. If you are already working with a contractor that is not authorized, they can apply to become authorized through Michigan Saves. More information on this authorized contractor application process is available at: https://michigansaves.org/contractors.

I’m still trying to determine whether to proceed with a solar or other qualifying project. Can someone from Michigan Saves guide me through the financing process and help find a contractor?

Yes. You should contact Michigan Saves at 517-484-6474 or info@michigansaves.org.

Additional Details on Investment Tax Credit

What is considered energy-property eligible for the investment tax credit (ITC)? How can I be sure that my project will qualify for direct pay?

The Department of Energy explains how energy property is calculated for the ITC:

[…] ITC is calculated based on the cost of building the system, so understanding what expenses are eligible to include is important in determining how much of a tax credit the system is eligible for.

To calculate the ITC, you multiply the applicable tax credit percentage by the “tax basis,” or the amount spent on eligible property. Eligible property includes the following:

- Solar PV panels, inverters, racking, balance-of-system equipment, and sales and use taxes on the equipment*;

- CSP [concentrating solar-thermal power] equipment necessary to generate electricity, heat or cool a structure, or to provide solar process heat;

- Installation costs and certain prorated indirect costs;

- Step-up transformers, circuit breakers, and surge arrestors**;

- Energy storage devices that have a capacity rating of 5 kilowatt hours or greater (even if not charged with solar)

- For projects 5 MW or less, the tax basis can include the interconnection property costs spent by the project owner to enable distribution and transmission of the electricity produced or stored by the system—this can include costs that are incurred beyond the point at which the energy property interconnects to the distribution or transmission systems.

The cost of a roof installation is generally not eligible, except for incremental costs, or the amount over what you would have spent if the roof was not used for solar. These costs could include solar shingle, solar tiles, or the incremental cost of installing a reflective roof membrane that increases electricity generation.2

Michigan Saves strongly suggests that tax-exempt entities review the IRS regulations defining energy property (26 CFR Part 1.48-9 and 26 USC Part 48). Michigan Saves recommends referring to the IRS for details and/or seeking advice from an attorney or tax professional to verify amounts to claim under the direct pay provisions. Michigan Saves cannot guarantee eligibility or offer tax or legal advice.

*if the tax is capitalized and included in the depreciable basis of the asset (this includes rooftop, ground-mounted, and community solar systems).

**if such items are integral to the energy property’s function (i.e. do not serve a general utility purpose)

[2] US Department of Energy. August 2024. “Federal Solar Tax Credits for Businesses.” Energy.gov. https://www.energy.gov/eere/solar/federal-solar-tax-credits-businesses#_edn84

How much is the investment tax credit?

The ITC can range from 6 to 70 percent depending on the location, equipment origin, and other circumstances.

The ITC base credit is 30 percent of the installed cost for projects that meet the prevailing wage and apprenticeship requirements or are less than one megawatt in capacity for solar. For solar projects one megawatt or greater that do not meet these labor requirements, the base credit is only 6 percent. There is also the opportunity for additional tax credit adders, up to a total of 70 percent (30 percent base plus 40 percent in adders) under certain circumstances, as follows:

- 30 percent base ITC

- 10 percent domestic content adder

- 10 percent energy community adder

- Up to 20 percent for low-income communities adder

Unlike the base credit and other adders, the low-income communities adder is subject to available allocations of 1.8 GW per year nationally and therefore must be applied for and received to qualify. Awarded projects have four years to be placed into service . The low-income communities adder is either:

- 10 percent if the project is located in a low-income community (based on the New Markets Tax Credit Program definition) or tribal lands

- 20 percent if the project is for low-income community solar or federally supported multifamily housing under Section 8 or the Low-Income Housing Tax Credit

Where can I learn more about criteria to qualify for the ITC adders?

Federal reference information on the adders is available on the following websites:

- Domestic content:

- Energy communities:

- Official energy communities map: “Inflation Reduction Act Energy Community Tax Credit Bonus”

- IRS FAQs: “Frequently Asked Questions for Energy Communities” | Internal Revenue Service

- Low-income communities:

- IRS regulations and guidance: “Low-Income Communities Bonus Credit” | Internal Revenue Service

- IRS 48(e) Applicant User Guide: “Low-Income Communities Bonus Credit Program” | Internal Revenue Service

What are the steps for securing direct pay for the investment tax credit?

An important part of the process for securing direct pay is to complete the prefiling registration with the IRS. Please note that organizations must elect direct pay on their tax return for the year the credit is claimed. Prefiling registration is required to obtain the final advance of a Michigan Saves bridge loan. This added eligibility requirement ensures your tax-exempt entity is doing what is necessary to obtain the tax credits you are seeking In order to complete prefiling registration, visit the IRS registration portal (IRS Registration Portal) and either create an ID.me account or login to your existing account. Once logged in, select “Start a New Registration” and input the requested information, which includes information about the project and applicable credits. Once reviewed, the IRS will issue a registration number, which must be included on the organization’s tax return when claiming the credit with direct pay. The IRS review process may take several weeks to a few months, so it is important to give your entity adequate time to account for the lag time. Organizations should file for the pre-registration as soon as the project is placed-in-service.

How can I learn more about the investment tax credit?

For additional information about direct/elective pay, visit the IRS website: https://www.irs.gov/credits-deductions/elective-pay-and-transferability-frequently-asked-questions

Lawyers for Good Government has also published a user-friendly guide: https://www.lawyersforgoodgovernment.org/elective-pay-ira-tax-incentives